Democracy Forward Demands IG Investigation, Releases Trove of Records Revealing HUD’s Yearlong Charade

Administration’s Haphazard and Unlawful Actions Hurt DACA Recipients and Lenders, Created Uncertainty in Home Mortgage Market

Washington, D.C. — Today, Democracy Forward requested that the Department of Housing and Urban Development (HUD) Office of the Inspector General immediately investigate whether the Trump administration violated federal law by unlawfully implementing a secret policy to deny DACA recipients federally-backed housing loans. HUD also misled Congress about the policy change. Democracy Forward submitted over 150 pages of internal HUD records that show how the agency’s haphazard, nonpublic implementation of its DACA exclusion policy violated statutory requirements for agency decision-making, hurt HUD’s credibility, and created uncertainty in the home mortgage market. Those records can be found here.

“The Trump administration’s unacknowledged, unlawful decision to deny DACA recipients federal home loan eligibility hurt DACA recipients and lenders and created uncertainty in the home mortgage market,” said Democracy Forward Senior Counsel Robin Thurston. “It was an administrative trainwreck — and yet another example of what happens when the Trump administration’s disregard for immigrants and inability to govern collide.”

Democracy Forward’s records show that, following President Trump’s failed attempt to terminate the DACA program, HUD quietly determined — contrary to its historical practice — that DACA recipients do not meet the “lawful residency” requirement for Federal Housing Administration (FHA) loans. By relying on the U.S. Customs and Immigration Services’ position that DACA recipients lack “lawful status,” HUD wrongly concluded that DACA recipients similarly lack “lawful residence” and are therefore ineligible for FHA loans. HUD reached this conclusion despite the fact that U.S. Citizenship and Immigration Services acknowledges that DACA recipients are lawfully present in the country. This change was quietly codified internally through unpublished November 2018 agency guidance.

HUD officials then executed their new DACA exclusion policy in secret, sowing confusion among lenders and violating federal law that requires agencies to make policy-making decisions available to the public. Documented evidence reveals that:

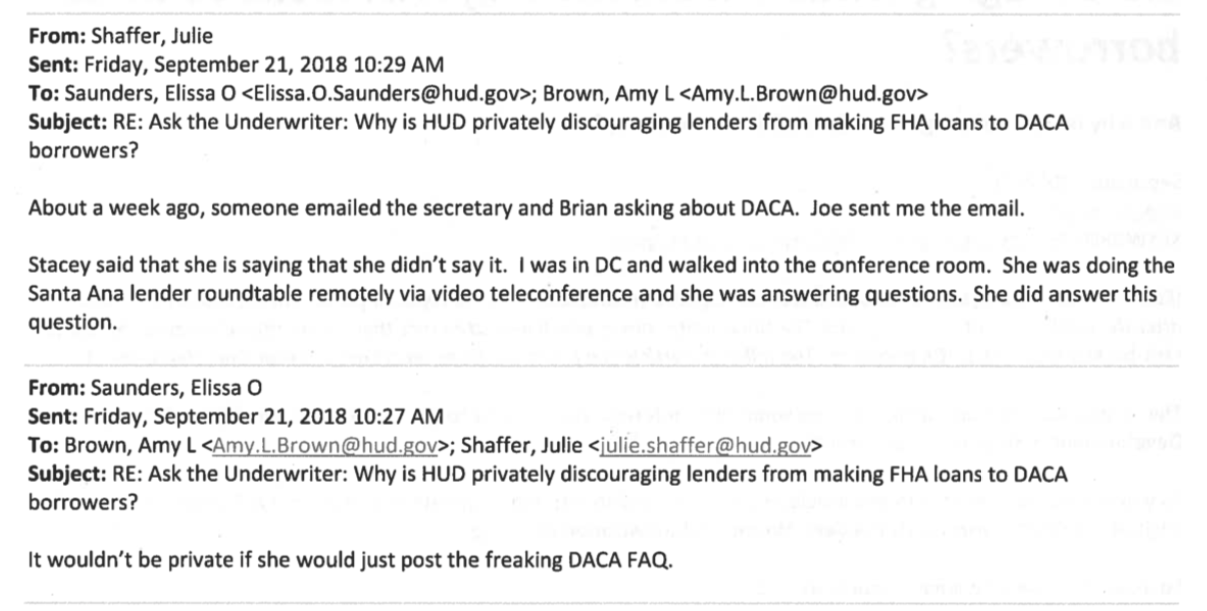

- HUD verbally conveyed the policy change to individual lenders on an ad hoc basis, frustrating some lenders who insisted to HUD officials that the agency’s “policy needs to be announced officially.” HUD staff also expressed frustration that senior leadership would not “post the freaking DACA [Frequently Asked Questions],” which would have made the department’s policy clear and public.

{kind=link}

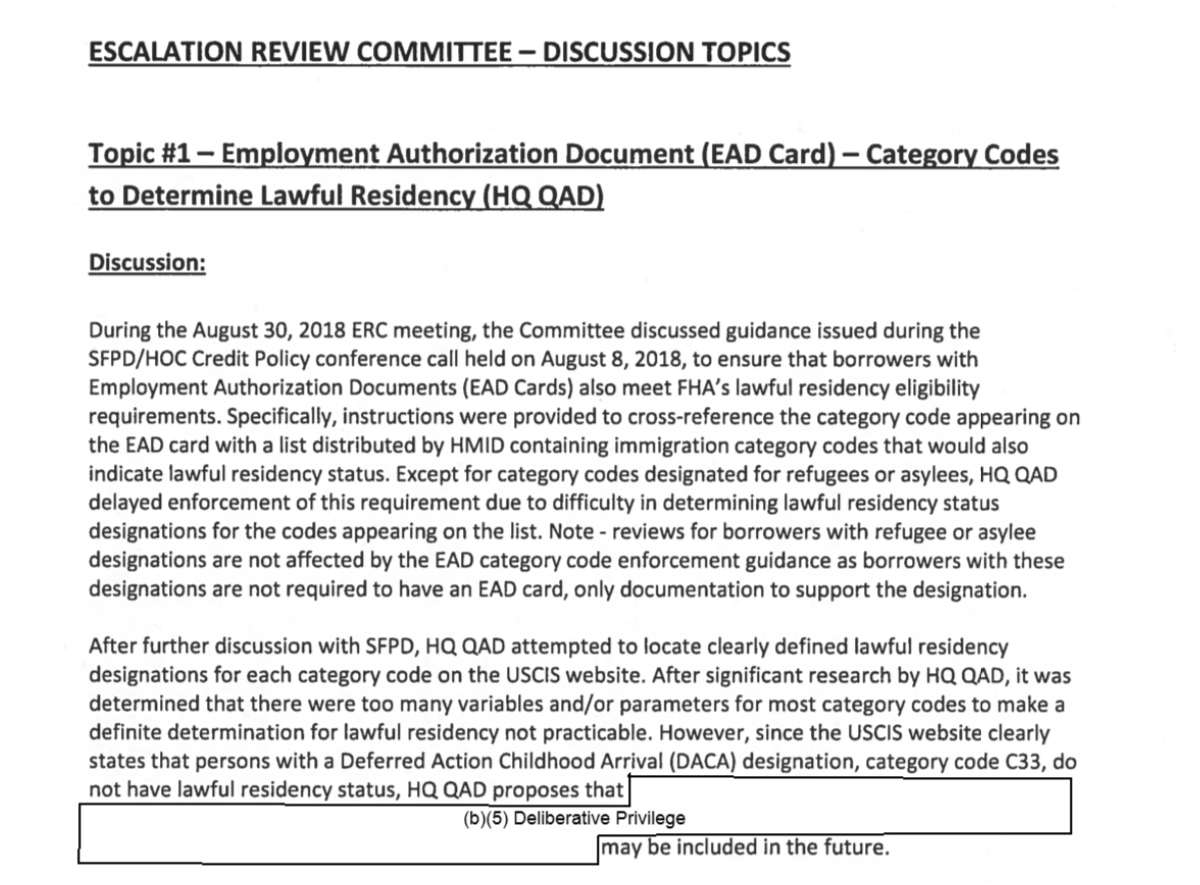

- During an August 2018 internal FHA policy call, HUD staff were instructed to apply the new “lawful residency” interpretation by excluding loan applicants who have work permits that contain an employment code reserved for DACA recipients. That instruction was later codified in November 2018 agency guidance.

{kind=link}

{kind=link}

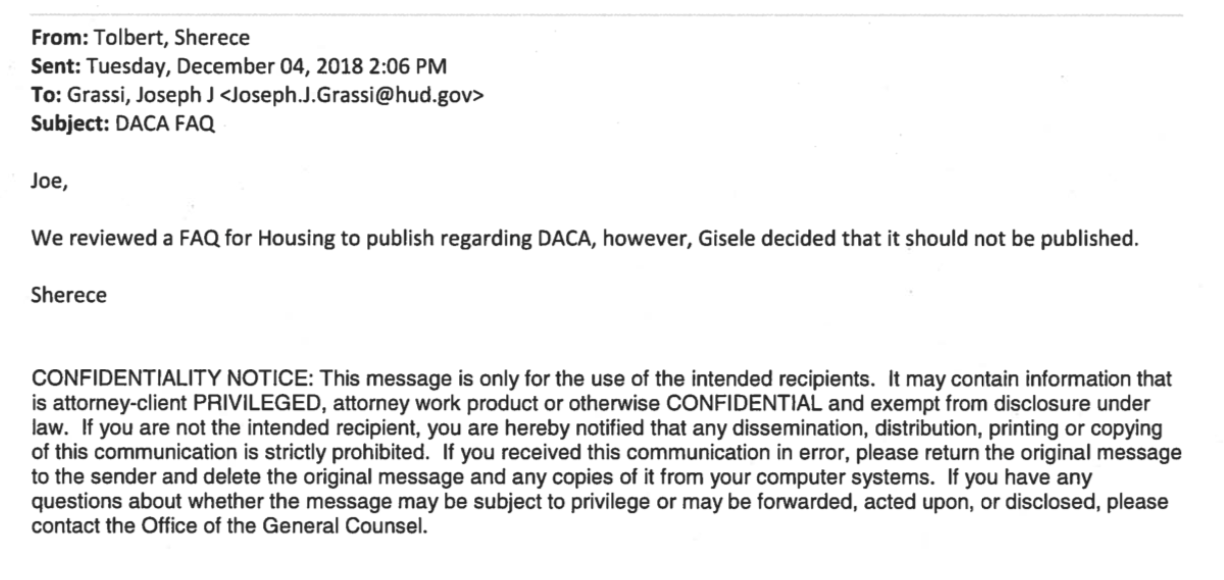

- HUD was well aware of its lack of transparency and candor. Indeed, HUD had drafted an FAQ for the public explaining its view on DACA eligibility as early as May 2018, but the FAQ was never published because, as one internal email exchange from December 2018 shows, a senior HUD official “decided that it should not be published.”

{kind=link}

Records also reveal the extent to which the agency misled Congress. After Senators Menendez, Booker, Cortez Masto and House Financial Services Committee Chair Waters and other Representatives pressed HUD in December 2018 and Rep. Pete Aguilar pressed again in May 2019 to provide answers about the reported change in policy, Secretary Ben Carson and other HUD officials — including Asst. Sec Len Wolfson and FHA Commissioner Brian Montgomery — claimed they weren’t aware of any policy change “either formal or informal.” Indeed, HUD leadership consistently doubled down on their denial that HUD policy was changed to bar DACA recipients from receiving FHA loans. It wasn’t until a June 2019 response to Rep. Aguilar that HUD announced, for the first time in writing, that DACA recipients lack eligibility for FHA-backed loans. But the announcement did not acknowledge that Trump’s HUD made this change. That position was reiterated in a July 2019 response to a letter led by Rep. Juan Vargas. Most glaringly, records reveal that:

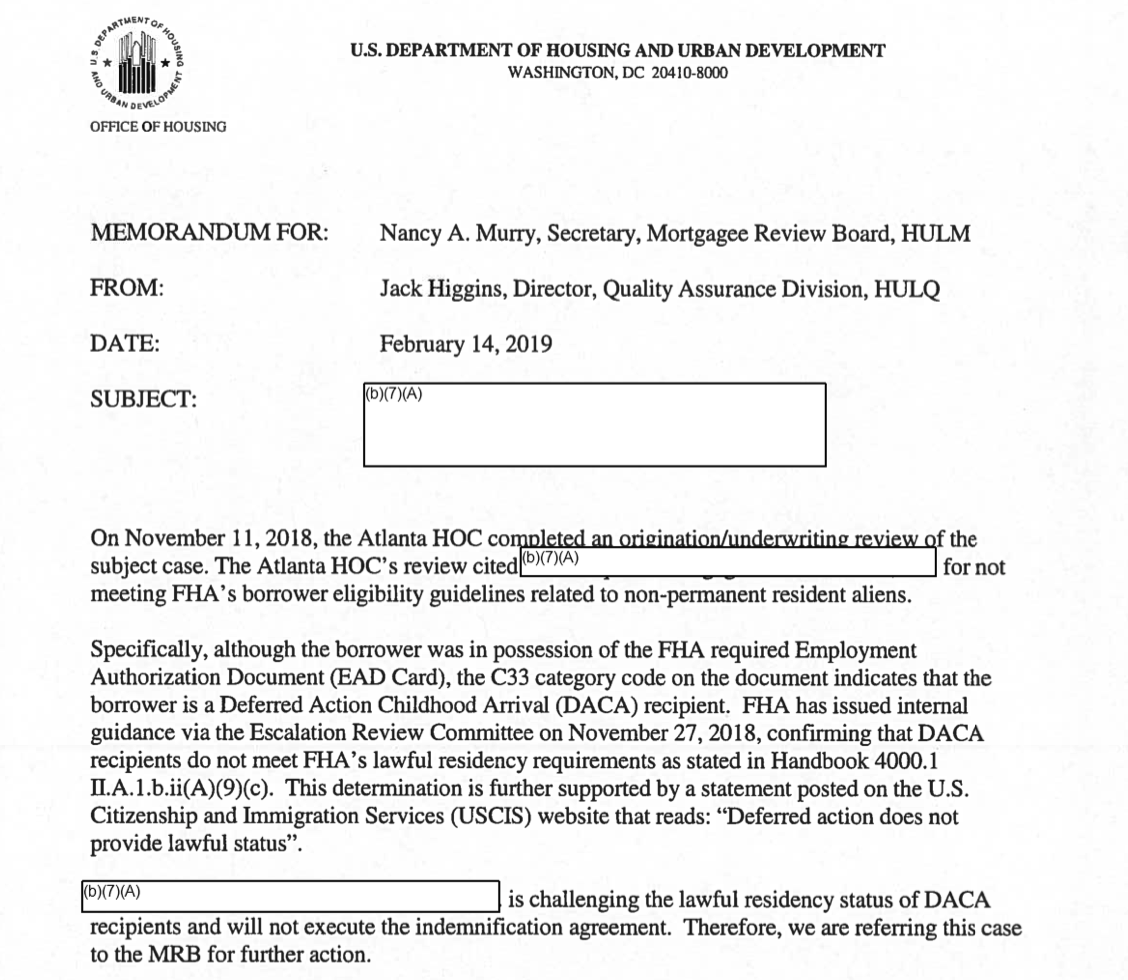

- In February 2019, FHA Administrator Brian Montgomery told a House subcommittee there was no change in policy despite being aware that HUD had, indeed, changed its policy to bar DACA recipients from receiving FHA loans. In answer to a question by Rep. Aguilar, Montgomery replied under oath that the DACA “policy has been unchanged for many years.” He added: “ I can’t speak for all of my staff, but I do know we haven’t changed that policy dating back 15 years or so.” But records show that Montgomery received an email in July 2018 regarding HUD’s interpretation of its “lawful residency” requirement and conclusion that DACA recipients were ineligible. Indeed, Montgomery had asked for a meeting on the matter because “it comes up all the time” and was in possession of the draft FAQ on the policy change by December 2018.

{kind=link}

- In April 2019, HUD Sec. Carson testified before the House subcommittee that it would “surprise” him if DACA recipients were being turned away and that he’d “inquired of the appropriate people, including the FHA commissioner, and no one was aware of any changes that had been made to the policy whatsoever.” Records, however, suggest he spoke with Montgomery in the prior fall about the department’s instructions to lenders to exclude DACA recipients.

The Department has not taken any further steps to formally codify its DACA exclusion policy through a lawful policymaking process nor has it acknowledged the Trump Administration’s role in changing the policy to exclude DACA recipients.

The Federal Housing Administration is the largest mortgage insurer in the world — with an active insurance portfolio of over $1.3 trillion — and is crucial to expanding home ownership to first-time and low-income homeowners. FHA’s mortgage insurance provides lenders with protection against losses if a property owner defaults on a mortgage, allowing lenders to accept lower minimum down payments and credit scores than many conventional loans.

FHA-backed loans are particularly popular with low-to-moderate income first-time homebuyers and are often well suited to DACA recipients. Indeed, many DACA recipients have bought homes. Survey data shows that 14% of DACA recipients purchased their first home after acquiring DACA status.

The DACA program was established in 2012, protecting from deportation certain classes of undocumented residents who had come to the U.S. as children. President Trump rescinded the program in 2017, but multiple courts ordered the administration to allow current recipients to keep their status while allowing the administration to put a pause on new applications. The Supreme Court is set to rule on the program before its Summer 2020 recess.

The letter to Housing and Urban Development Inspector General Rae Oliver Davis was sent on June 5, 2020. Read the letter here.

###

Democracy Forward is a nonprofit legal organization that scrutinizes Executive Branch activity across policy areas, represents clients in litigation to challenge unlawful actions, and educates the public when the White House or federal agencies break the law.

Press Contact:

Charisma Troiano

(202) 701-1781

ctroiano@democracyforward.org